GST Calculator

Not sure if you need to register for GST? See our guide to the $60,000 GST registration threshold. Need to calculate income tax as well? Try our PAYE calculator.

Extraction method: The Minus GST calculation uses the IRD-prescribed 3/23 fraction, as set out in the Goods and Services Tax Act 1985. This avoids recurring-decimal rounding errors that arise from simply dividing by 1.15.

Registration threshold: $60,000 rolling 12-month turnover, per section 51 of the GST Act 1985.

Last verified: 1 April 2026, against the most recent IRD Tax Information Bulletin and current Inland Revenue guidance.

Source data: Inland Revenue (ird.govt.nz/gst) and the GST Act 1985.

The Goods and Services Tax (GST) in New Zealand is a comprehensive value-added tax applied to most products and services. Introduced on 1 October 1986 by the Fourth Labour Government at a rate of 10%, GST was raised to 12.5% in 1989 and then to 15% by the National government in 2010. This tax, primarily managed by the Inland Revenue Department, is usually filed every one, two, or six months, depending on the business's preference.

GST Registration and Returns for NZ Businesses

For businesses operating in New Zealand, registering for GST with the IRD is mandatory when the turnover exceeds $60,000. However, businesses with lower turnovers can opt for voluntary registration. GST registration is crucial, especially for businesses exporting goods and services, as they can zero-rate their exports. This means they charge GST at a 0% rate, allowing them to claim back the input GST on their returns. It's important to note that businesses providing GST-exempt supplies cannot claim back input GST.

Impact of GST on Business Operations

Understanding the base sales price excluding GST is essential for businesses, as it allows them to calculate the net GST they need to pay or claim back. The shift to a 15% GST rate has implications for cash flow, affecting how businesses manage their finances. Wholesalers, for example, often display prices without GST but charge the total amount, including tax, at the point of sale.

Simple Guide to Calculating GST in New Zealand

Calculating GST in New Zealand remains straightforward despite the rate change. The calculation is based on the 'base' value - the price excluding GST for adding GST, or the total price including GST for determining the tax component. For simplicity, let's consider a base value of $100 in our examples. This approach helps in understanding the process of calculating GST for different scenarios.

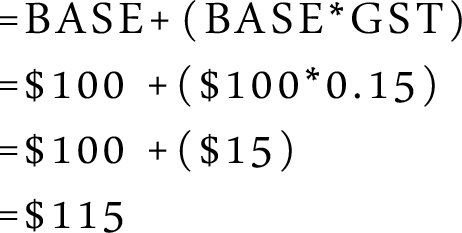

Addition of GST:

In the example you see below, we have started with a base figure of $100. Given that the rate of GST that we are using is 15% (which is written as 0.15 as a decimal) we can see that in this example we have the base ($100) and to that we have to add the GST of the original amount which in this case is (15% of $100). From that point, all we have to do is add the new found GST content ($15) to the base figure ($100) to get the new GST inclusive figure of $115.

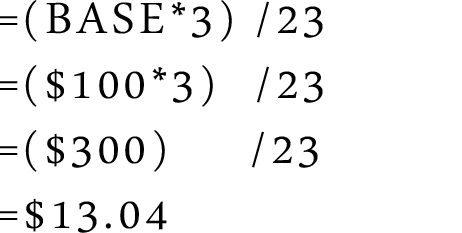

Finding GST Content:

In the example below, we can see that this calculation is slightly harder, but using the formula can be found quite easily. The base in this example is $100 again. Firstly we can see that overall the formula is GST Content =((BASE*3)/23) which on $100 is $13.04.

Here is an additional GST calculation example using real New Zealand GST incurring transactions.

GST Calculation Example 1: Andrew runs a small business doing building work, and during January he spent four weeks working on four different projects. These projects were for his building service only and did not include the supply of the building materials to do the job. In this example, we will calculate how much GST Andrew has collected during the period via the business contracting work.

In the first week, Andrew worked for $70 + GST per hour, for 50 hours. In the second week, Andrew worked for $85 + GST per hour, for 40 hours. In the third week, he worked for $75 + GST per hour for 45 hours, and in the last week, he worked for $70 + GST for 25 hours.

Week 1: $70.00 * 50 = $3,500 GST exclusive sub-total. GST exclusive sub-total $3,500 * 0.15 (15% GST rate) = $525.00, which is the GST content.. Adding those together the GST-inclusive total for the week = $4,025.00.

Week 2: $85.00 * 40 = $3,400 GST exclusive sub-total. GST exclusive sub-total $3,400 * 0.15 (15% GST rate) = $510.00, which is the GST content. Adding those together the GST-inclusive total for the week = $3,910.00.

Week 3: $75.00 * 45 = $3,375 GST exclusive sub-total. GST exclusive sub-total $3,375 * 0.15 (15% GST rate) = $506.25, which is the GST content. Adding those together the GST-inclusive total for the week = $3,881.25.

Week 4: $70.00 * 25 = $1,750 GST exclusive sub-total. GST exclusive sub-total $1,750 * 0.15 (15% GST rate) = $262.50, which is the GST content. Adding those together the GST-inclusive total for the week = $2,012.50.

Month Total = $12,025 GST exclusive sub-total. GST exclusive sub-total $12,025.00 * 0.15 (15% GST rate) = $1,803.75, which is the GST content. Adding those together the GST-inclusive total for the week = $13,828.75.

In this example, Andrew has collected through the sale of services $1,803.75 worth of GST which is the tax on the supply (sale) of the services that Andrew has undertaken in the period. If Andrew has a monthly GST return filing frequency, then that value would be the GST collected total. NOTE: Andrew would likely have purchases such as fuel and other services needed to complete this work which he may be eligible to offset this collected total via the GST that he has paid for the associated purchases and business expenses.

In the first week, Susan worked for $80 + GST per hour, for 30 hours. In the second week, Susan worked for $95 + GST per hour, for 35 hours. In the third week, she worked for $85 + GST per hour for 40 hours, and in the last week, she worked for $90 + GST for 20 hours.

Week 1: $80.00 * 30 = $2,400 GST exclusive sub-total. GST exclusive sub-total $2,400 * 0.15 (15% GST rate) = $360.00, which is the GST content. Adding those together the GST-inclusive total for the week = $2,760.00.

Week 2: $95.00 * 35 = $3,325 GST exclusive sub-total. GST exclusive sub-total $3,325 * 0.15 (15% GST rate) = $498.75, which is the GST content. Adding those together the GST-inclusive total for the week = $3,823.75.

Week 3: $85.00 * 40 = $3,400 GST exclusive sub-total. GST exclusive sub-total $3,400 * 0.15 (15% GST rate) = $510.00, which is the GST content. Adding those together the GST-inclusive total for the week = $3,910.00.

Week 4: $90.00 * 20 = $1,800 GST exclusive sub-total. GST exclusive sub-total $1,800 * 0.15 (15% GST rate) = $270.00, which is the GST content. Adding those together the GST-inclusive total for the week = $2,070.00.

Month Total = $10,925 GST exclusive sub-total. GST exclusive sub-total $10,925.00 * 0.15 (15% GST rate) = $1,638.75, which is the GST content. Adding those together the GST-inclusive total for the month = $12,563.75.

In this example, Susan has collected through the sale of services $1,638.75 worth of GST, which is the tax on the supply (sale) of the services that Susan has undertaken in the period. If Susan has a monthly GST return filing frequency, then that value would be the GST collected total. NOTE: Susan would likely have purchases such as software licenses and other services needed to complete this work, which she may be eligible to offset this collected total via the GST that she has paid for the associated purchases and business expenses.

GST Calculation Example 3: John runs a medium-sized construction company in New Zealand and during April, he spent four weeks working on four different projects. These projects included both labour and the supply of building materials. In this example, we will calculate how much GST John has collected during the period via the business contracting work, as well as how much GST was spent on necessary materials, using the New Zealand GST rate of 15%.

Project 1: Constructing a residential home - Labour: $50,000 + GST; Building materials: $150,000 + GST

Project 1 Labour: $50,000 * 0.15 (15% GST rate) = $7,500 GST content. GST-inclusive total = $57,500.

Project 1 Materials: $150,000 * 0.15 (15% GST rate) = $22,500 GST content. GST-inclusive total = $172,500.

Project 2: Renovating an office space - Labour: $25,000 + GST; Building materials: $75,000 + GST

Project 2 Labour: $25,000 * 0.15 (15% GST rate) = $3,750 GST content. GST-inclusive total = $28,750.

Project 2 Materials: $75,000 * 0.15 (15% GST rate) = $11,250 GST content. GST-inclusive total = $86,250.

Project 3: Repairing a warehouse roof - Labour: $15,000 + GST; Building materials: $35,000 + GST

Project 3 Labour: $15,000 * 0.15 (15% GST rate) = $2,250 GST content. GST-inclusive total = $17,250.

Project 3 Materials: $35,000 * 0.15 (15% GST rate) = $5,250 GST content. GST-inclusive total = $40,250.

Project 4: Building a garden shed - Labour: $5,000 + GST; Building materials: $10,000 + GST

Project 4 Labour: $5,000 * 0.15 (15% GST rate) = $750 GST content. GST-inclusive total = $5,750.

Project 4 Materials: $10,000 * 0.15 (15% GST rate) = $1,500 GST content. GST-inclusive total = $11,500.

Month Total Labour = $95,000 GST exclusive sub-total. GST exclusive sub-total $95,000 * 0.15 (15% GST rate) = $14,250, which is the GST content. Adding those together, the GST-inclusive total for labour = $109,250.

Month Total Materials = $270,000 GST exclusive sub-total. GST exclusive sub-total $270,000 * 0.15 (15% GST rate) = $40,500, which is the GST content. Adding those together, the GST-inclusive total for materials = $310,500.

In this example, John has collected through the sale of services and materials $54,750 worth of GST ($14,250 from labour and $40,500 from materials), which is the tax on the supply (sale) of the services and materials that John has undertaken in the period. If John has a monthly GST return filing frequency, then that value would be the GST collected total.

During the same period, John spent the following amounts on purchasing necessary items to complete the projects:

- Equipment rental: $20,000 + GST

- Fuel for vehicles: $5,000 + GST

- Office supplies: $1,000 + GST

Equipment Rental: $20,000 * 0.15 (15% GST rate) = $3,000 GST content. GST-inclusive total = $23,000.

Fuel for vehicles: $5,000 * 0.15 (15% GST rate) = $750 GST content. GST-inclusive total = $5,750.

Office supplies: $1,000 * 0.15 (15% GST rate) = $150 GST content. GST-inclusive total = $1,150.

Month Total Expenses = $26,000 GST exclusive sub-total.

GST exclusive sub-total $26,000 * 0.15 (15% GST rate) = $3,900, which is the GST content. Adding those together, the GST-inclusive total for expenses = $29,900.

In this example, John has paid $3,900 worth of GST on the necessary items to complete the projects. This amount can be offset against the $54,750 GST collected total to determine the net GST payable.

Net GST Payable = GST Collected - GST Paid on Expenses Net GST Payable = $54,750 - $3,900 = $50,850

In this more detailed example, John has a net GST payable of $50,850 for the period. This is the amount of GST he is required to remit to the New Zealand IRD when he files his monthly GST return. By providing a more elaborate breakdown of labour, materials, and expenses, this example showcases a more comprehensive approach to calculating NZ GST for a construction company, accounting for both GST collected and spent on items needed to complete the job.

GST Calculation Example 4: Tim is a private fisherman who sells his high quality Snapper catch to various local seafood restaurants in the coatal town on Paihia. In December, he completed several deliveries to his clients but did not receive any payments from them in that month. He did, however, incur costs for the services needed to run his fishing operation during December. In this example, we will calculate Tim's GST obligations for December, considering the unpaid sales and the expenses incurred.

Sales:

Week 1: 3,000 kg of fish * $15/kg = $45,000

Week 2: 2,500 kg of fish * $15/kg = $37,500

Week 3: 4,000 kg of fish * $15/kg = $60,000

Week 4: 3,500 kg of fish * $15/kg = $52,500 Total Sales (GST-exclusive): $195,000

Tim did not receive any payments for his sales in December, so his GST collected for the month is $0.

Expenses:

Boat fuel: $12,000 * 0.15 (15% GST rate) = $1,800 GST content. GST-inclusive total = $13,800.

Fishing gear maintenance: $8,000 * 0.15 (15% GST rate) = $1,200 GST content. GST-inclusive total = $9,200.

Bait: $6,000 * 0.15 (15% GST rate) = $900 GST content. GST-inclusive total = $6,900.

Month Total Expenses = $26,000 GST-exclusive sub-total. GST-exclusive sub-total $26,000 * 0.15 (15% GST rate) = $3,900, which is the GST content. Adding those together, the GST-inclusive total for expenses = $29,900.

In this example, Tim has paid $3,900 worth of GST on the necessary items to run his fishing operation in December. Since he did not receive any payments for his sales, his GST collected total for the month is $0. As a result, Tim has a net GST credit for December.

Net GST Credit = GST Collected - GST Paid on Expenses Net GST Credit = $0 - $3,900 = -$3,900

In this case, Tim has a net GST credit of $3,900 for the period. This means he can claim a refund when he files his monthly GST return with the IRD. This example demonstrates how a business that makes sales but does not receive payment in a given month can still account for GST paid on expenses incurred during that period.

GST Calculation Example 5: Sarah, an independent graphic designer in Wellington, New Zealand, had various clients and expenses in May. She invoiced her clients for design services and incurred several business-related expenses. In this example, we'll calculate Sarah's GST obligations for May, considering both the GST on her services and the GST on her expenses.

Sales (Services Provided):

Week 1: Branding project for a cafe - $4,000 + GST

Week 2: Website design for a local artist - $6,000 + GST

Week 3: Marketing material design for a charity event - $3,500 + GST

Week 4: Packaging design for a small business - $5,500 + GST Total Sales (GST-exclusive): $19,000

Each service incurs 15% GST, so:

Week 1 Service: $4,000 * 0.15 = $600 GST content. GST-inclusive total = $4,600.

Week 2 Service: $6,000 * 0.15 = $900 GST content. GST-inclusive total = $6,900.

Week 3 Service: $3,500 * 0.15 = $525 GST content. GST-inclusive total = $4,025.

Week 4 Service: $5,500 * 0.15 = $825 GST content. GST-inclusive total = $6,325.

Total GST Collected: $2,850 (Sum of GST contents for all services)

Expenses:

Computer software subscription: $300 * 0.15 (15% GST rate) = $45 GST content. GST-inclusive total = $345. Office rent: $1,200 * 0.15 (15% GST rate) = $180 GST content. GST-inclusive total = $1,380. Printing and materials: $700 * 0.15 (15% GST rate) = $105 GST content. GST-inclusive total = $805. Total Expenses (GST-exclusive): $2,200 Total GST Paid on Expenses: $330 (Sum of GST contents for all expenses)

Net GST Calculation:

Net GST Payable = GST Collected - GST Paid on Expenses Net GST Payable = $2,850 - $330 = $2,520

In this scenario, Sarah has a net GST payable of $2,520 for May. She collected $2,850 in GST through her design services but also paid $330 in GST on business-related expenses. This means, for her May operations, Sarah will need to remit $2,520 to the New Zealand Inland Revenue Department (IRD) as part of her GST return. This example highlights the importance for small business owners, like independent graphic designers, to accurately track both their income and expenses for effective GST management. Understanding these calculations helps ensure compliance with New Zealand's tax regulations and aids in maintaining a clear financial picture of the business.

Common Business Expenses That May Incur GST in New Zealand

Most ordinary business purchases made by a GST-registered business in New Zealand will include GST, which can usually be claimed back as an input tax credit when you file your GST return. Common categories include:

- Premises and utilities: commercial rent, power, gas, water, internet, and mobile phone bills.

- Equipment and supplies: tools, machinery, office furniture, raw materials, packaging, and day-to-day consumables.

- Professional services: accounting, legal fees, tax preparation, consulting, and business coaching.

- Marketing and advertising: digital ads, SEO, social media management, design, print materials, and sponsorships.

- Technology: software subscriptions, cloud services, website hosting, domain names, and app licences.

- Transport and logistics: fuel, vehicle maintenance, freight, courier services, and customs brokerage.

- Staff-related costs: uniforms, safety gear, training, and work-related travel (note: entertainment and fringe benefits have specific rules).

- Insurance: most business insurance premiums (but not life insurance, which is GST-exempt).

Not everything is claimable. Residential rent, most financial services, and donated goods sold by non-profits are GST-exempt. Mixed-use expenses (for example, a vehicle used 60% for business) can only have the business-use portion claimed. If you are unsure, check directly with Inland Revenue or a registered tax agent.

Who this GST calculator is for

This calculator is for anyone in New Zealand who needs to add or remove 15% GST. That includes small business owners and sole traders pricing goods and services, freelancers and contractors invoicing clients, bookkeepers and accountants checking figures, and shoppers who simply want to see the GST content of a price. It works for GST-registered businesses calculating what to charge or claim back, and for consumers wanting the tax portion of a total.

What this calculator assumes

- A GST rate of 15%, the rate in force in New Zealand since 1 October 2010.

- The amount you enter is either fully GST-exclusive or fully GST-inclusive, as you select, not a mix of the two.

- The supply is a standard taxable supply, not a zero-rated or GST-exempt one, which are treated differently.

- Results are indicative and rounded for display; your filed GST return should rely on your own accounting records.

Frequently Asked Questions about NZ GST

What is the current GST rate in New Zealand?

The current GST rate in New Zealand is 15%. It has been 15% since 1 October 2010, when it was raised from 12.5%. There is no scheduled change for the 2026/27 tax year.

How do I add GST to a price?

Multiply the GST-exclusive price by 1.15. For example, $500 plus GST is $500 × 1.15 = $575. The GST component is $75.

How do I remove GST from a GST-inclusive total?

Use the IRD-prescribed 3/23 fraction. Multiply the GST-inclusive total by 3 and divide by 23. For example, $575 × 3 ÷ 23 = $75 GST. The GST-exclusive amount is $575 − $75 = $500. This is the official method under the GST Act 1985 and avoids the rounding drift that occurs if you simply divide by 1.15. See our dedicated Reverse GST Calculator for a full explanation of the method and worked examples.

Why does 15% of a GST-inclusive price give the wrong answer?

A very common mistake. If a product costs $115 including GST, taking 15% of $115 gives $17.25, which is incorrect. The actual GST is $15, found by dividing $115 by 1.15, or by applying the 3/23 fraction ($115 × 3 ÷ 23 = $15).

When do I have to register for GST?

Registration is mandatory once your turnover exceeds $60,000 on a rolling 12-month basis, under section 51 of the Goods and Services Tax Act 1985. The threshold does not reset each financial year. Voluntary registration below this threshold is permitted and can be useful for businesses with high input costs or who primarily supply other GST-registered businesses. For full details on the test, including worked monthly examples and voluntary registration, see our guide to the GST Registration Threshold. Tradies in particular should read our GST for Tradies guide, which covers registration decisions for builders, electricians, plumbers, and subcontractors.

Does GST apply to imports?

Yes. Since 1 December 2019, GST applies to all goods imported into New Zealand regardless of value. For goods valued over $1,000, NZ Customs collects GST at the border using the formula (Customs value + Freight + Insurance + Customs duty) × 15%. For goods valued at $1,000 or less, overseas sellers are generally required to collect GST at the point of sale. Our GST on Imports guide covers the Customs formula, the low-value imported goods rules, remote services GST, and how to claim import GST back.

What is the difference between zero-rated and GST-exempt?

Zero-rated supplies are taxed at 0% GST, but the supplier can still claim input GST credits on related expenses. Typical examples include exported goods and services. GST-exempt supplies, such as residential rent and most financial services, do not allow the supplier to claim GST on related expenses.

How often do I need to file a GST return?

Filing frequency depends on turnover: monthly (mandatory over $24 million), two-monthly (the default for most small and medium businesses), or six-monthly (available for businesses under $500,000 turnover). Returns and payment are generally due by the 28th of the month following the end of the taxable period, with some exceptions for November and March periods. For the complete schedule of deadlines for the 2026/27 tax year across all three filing frequencies, see our GST Due Dates 2026/27 page.

Can I use this calculator for the pre-2010 12.5% rate or Australian GST?

Yes. The GST percentage field accepts any rate. Enter 12.5 for the historical NZ rate that applied from 1989 to 2010, or 10 for the current Australian GST rate.

Related NZ Tax and Business Calculators

Calculate.co.nz maintains over 150 calculators, all reviewed and updated in line with current New Zealand legislation. The following in-depth guides and calculators cover the most common GST topics in detail:

Deeper GST Guides

- Reverse GST Calculator: extract the 15% GST content from any GST-inclusive total using the IRD 3/23 fraction method.

- GST on Imports: how the 15% Customs formula works, the $1,000 threshold, and remote services GST.

- GST Due Dates 2026/27: complete deadline schedule for monthly, two-monthly, and six-monthly filers.

- GST Registration Threshold: the $60,000 rolling 12-month rule explained, plus voluntary registration.

- GST for Tradies: practical GST guide for builders, electricians, plumbers, and subcontractors.

Other Tax and Business Calculators

- PAYE Calculator: take-home pay after income tax, ACC levy, KiwiSaver and student loan deductions for the 2026/27 year.

- Business GST Calculator: net GST payable across multiple sales and expense lines.

- Business Income Tax Calculator: company and sole-trader income tax estimation.

- Australian GST Calculator: dedicated 10% Australian GST calculator.

- Income Tax Calculator: NZ personal income tax at 2026/27 rates.

- FBT Calculator: Fringe Benefit Tax on employee benefits.

- Selling Price Calculator: set prices that factor in GST and target margin.

- Profit Margin Calculator: GST-exclusive margin analysis.

- Discount Calculator: sale pricing with GST handling.

- ESCT Calculator: Employer Superannuation Contribution Tax.

For property-related GST questions, where treatment can be complex (commercial property, subdivisions, going-concern sales, and the change-of-use rules), calculate.co.nz is part of the Realtor.co.nz group, providing comprehensive guidance across the full NZ property transaction lifecycle.

Related calculators

- Best Start Payment Calculator

- Overseas-Based Student Loan Repayment Calculator

- KiwiSaver Retirement Projection Calculator

- NZ Super Rate Calculator

- Bright-Line Test Date Calculator

- Rental Interest Deductibility Calculator

Official NZ sources

This calculator is built from primary New Zealand sources. Always confirm current figures against the official source for your situation:

- Inland Revenue (IRD) – GST overview, the 15% rate and how GST works

- Inland Revenue (IRD) – registering for GST and the $60,000 turnover threshold

- Inland Revenue (IRD) – filing and paying GST returns

If you've found a bug, or would like to contact us, or learn more about James Graham and Calculate.co.nz.

Calculate.co.nz is partnered with Interest.co.nz for New Zealand's highest quality calculators and financial analysis.

Calculate.co.nz is the sister site of CalculatorHub.com, the world's largest calculator website by tool count.

All calculators and tools are provided for educational and indicative purposes only and do not constitute financial advice.

Calculate.co.nz is proudly part of the Realtor.co.nz group, New Zealand's leading property transaction literacy platform, helping Kiwis understand the home buying and selling process from start to finish. Whether you're a first home buyer navigating your first property purchase, an investor evaluating your next acquisition, or a homeowner planning to sell, Realtor.co.nz provides clear, independent, and trustworthy guidance on every step of the New Zealand property transaction journey.

Calculate.co.nz is also partnered with Health Based Building and Premium Homes to promote informed choices that lead to better long-term outcomes for Kiwi households.

Calculate.co.nz is hosted in Auckland via SiteHost new Zealand.

All content on this website, including calculators, tools, source code, and design, is protected under the Copyright Act 1994 (New Zealand). No part of this site may be reproduced, copied, distributed, stored, or used in any form without prior written permission from the owner.

About & trust: Why Calculate is NZ's most comprehensive · By the Numbers · How we compare · Editorial standards · How we keep data current · NZ finance glossary · Research & data · Financial literacy NZ · About · Privacy policy · Terms of use

Reviewed and maintained. Last reviewed 2026-07-02 and checked on a twice-monthly cycle against IRD, RBNZ and Stats NZ. How we keep data current.

© 2026 Calculate.co.nz. All rights reserved. Building free NZ calculators since 2011.